Why Do I Have to Insure My Home for More Than It’s Worth?

A question we often hear from homeowners in Alabama is: “Why do I have to insure my home for more than it’s worth?”

At first glance, it feels backwards. If your home would sell for $275,000 or $300,000, why is your insurance company requiring you to insure it for $450,000 or even $600,000? The short answer is that home insurance doesn’t factor what your home is worth, or its value, insurance is based on what it would cost to rebuild the home today.

???? As insurance advisors, we work closely with our customers to ensure their homes are accurately insured. Our goal isn’t to insure your home for the highest number possible — it’s to insure it correctly, and educate our clients. We don’t blindly accept insurance company changes. Instead, we work with our clients and the carriers to make sure homes are properly insured while still receiving fair value in their insurance coverage.

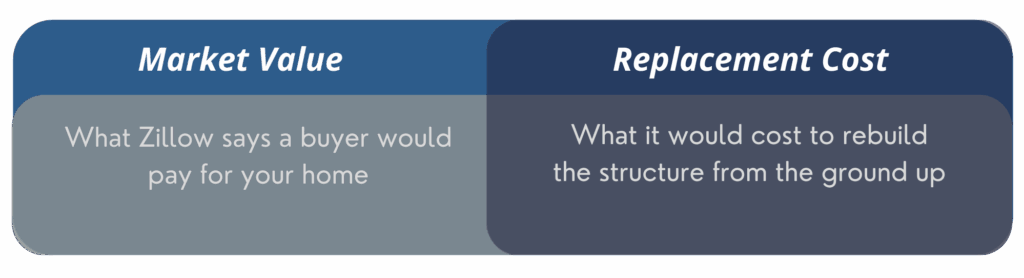

???? Market Value vs. Replacement Cost

Your home has two very different values: the Market value which is what Zillow says a buyer would pay for your home, and the Replacement cost which is what it would cost to rebuild the structure from the ground up.

Home insurance is based on replacement cost, not market value. When someone buys your home, they’re paying for: the house, the land, the location, the school districts, the market demand, and the comparable sales.

Insurance works differently. Land is not insured. Thankfully land does not burn down or suffer water damage. Insurance only covers the structure itself and what it would cost to rebuild it after a total loss.

???? Why This Comes Up So Often in Alabama

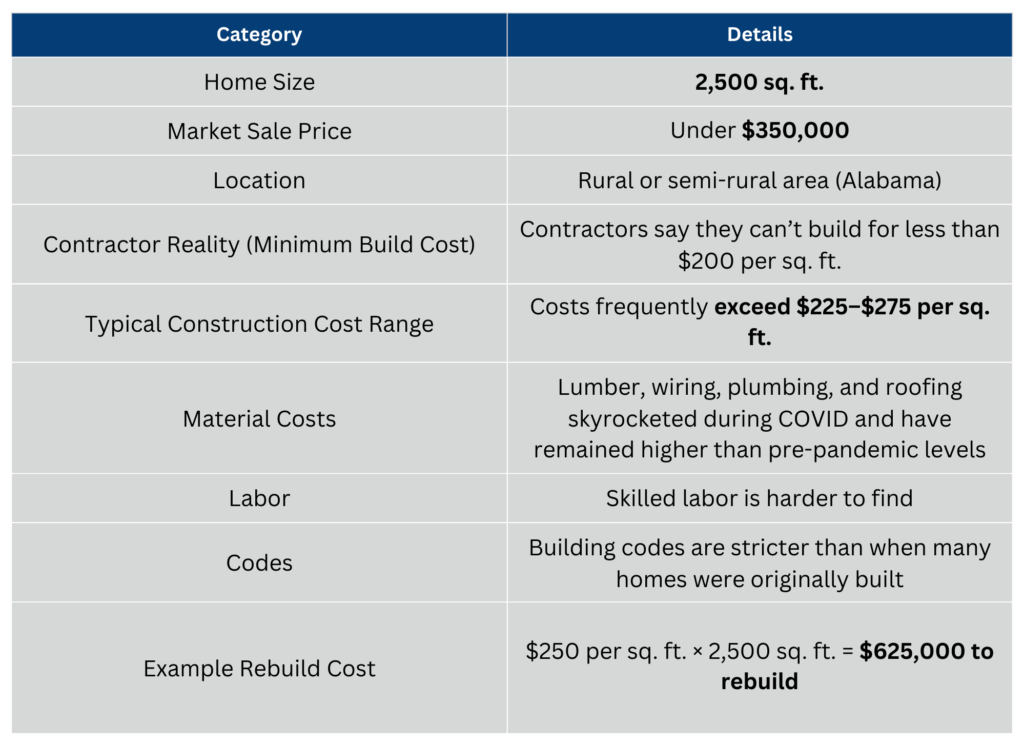

This question comes up frequently in Alabama, both in rural and semi-rural areas, where homes are often larger but still relatively affordable.

Here’s a real-world example we see regularly:

That’s why an insurance company may require the home to be insured for over $500,000, even though it would sell for much less.

❓ Do I Really Have to Insure the Building for That Much?

After a total loss, an insurance company’s obligation is not to pay what the home was “worth on the market.”

Their obligation is to rebuild the structure to its prior condition (or as close as possible). For this reason, the home must be insured for what it actually costs to rebuild.

If your home is underinsured and a total loss occurs:

-

???? The insurance company does not make up the difference

-

???? You could be left paying out of pocket

-

⚠️ Claims may be reduced due to underinsurance penalties

This is exactly the scenario insurance companies are trying to avoid — and why they are strict about replacement cost.

⛈️ Why Insurance Companies Are Getting Stricter

About 5 years ago we saw this issue become much more of a problem because several factors came together at the same time. We had a large number of big insurance claims (hurricanes, wildfires, floods), these events were more intense and cost more than prior years, and construction prices increased dramatically.

One major issue insurance companies identified at this time: many homes were insured for far less than it was actually costing to rebuild them.

As a result, carriers now:

-

???? Use detailed replacement cost estimators

-

???? Update construction pricing more frequently

-

???? Require higher dwelling limits

-

⛔ Decline or restrict underinsured policies

This isn’t about charging more premium — it’s about avoiding underinsurance when a loss occurs.

???? What This Means for Homeowners

It’s understandable to feel uncomfortable insuring your home for more than you paid for it. But the reality is this:

If your home were destroyed tomorrow, the rebuild cost — not the sale price — is what determines whether you are financially protected.

Proper insurance should feel boring and conservative. If the dwelling limit looks “too high,” it’s often because it’s actually realistic.

???? Our Role as Your Insurance Advisor

At our agency, we don’t blindly accept numbers from an insurance company. We:

-

Review replacement cost estimates

-

Adjust for quality, materials, and local conditions

-

Explain why a number is what it is

-

Push back against the insurance company when something doesn’t make sense

Our goal isn’t to insure your home for the highest number possible — it’s to insure it correctly, so you’re protected when it matters most.

If you’ve ever looked at your policy and thought, “This can’t be right,” you’re not alone — and it’s worth working with an advisor that’s looking out for you.

???? Talk With an Advisor: 205-738-7444

Please call us to speak with a friendly Allison Team member!

![]()

205-738-7444